As discussed by the community there appears to be strong demand to add wstETH as a collateral asset on Vesta.

Following the risk assessment posted by @plpmtech, we’ll provide additional information that will help draw a more complete picture of wstETH’s risk profile, and provide our assessment of the suggested parameters.

In this risk assessment we will provide detailed information about market risk along with our assessment of the following parameters: Liquidation Ratio, Debt Ceiling, Liquidation Penalty, Vesta Reference Rate.

Risk Assessment

Market Risk

The token has been trading on Arbitrum for a relatively short time period (5 months). We’ll use the historical data from the last year for its Ethereum counterpart to give more depth to this analysis.

Volatility

Let’s analyze the maximum drawdowns, the 1 hour volatility and 24 hour volatility of wstETH. All of these values are based on Chainlink historical price data.

Asset price volatility - Last month

| 1 hour volatility | 1 day volatility | |

| wstETH | 0.63% | 3.27% |

Asset price volatility - Last Year

| 1 hour volatility | 1 day volatility | |

| wstETH | 0.56% | 4.26% |

Maximum drawdowns - Last year

| 1 hour maximum drawdown | 1 day maximum drawdown | |

| wstETH | -9.46% | -28.01% |

Liquidity

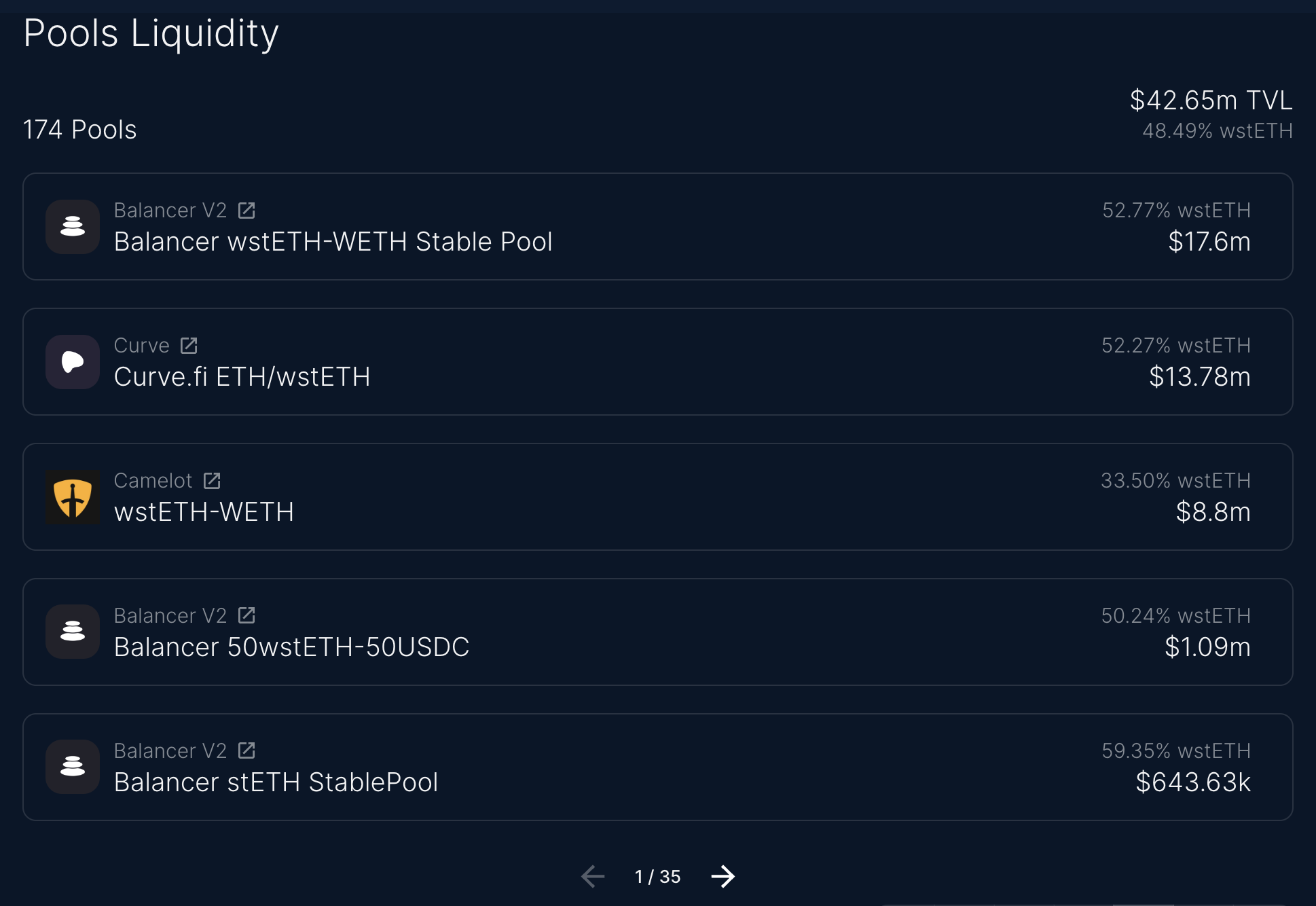

wstETH total DEX liquidity on Arbitrum has been ranging between 35M and 55M over the last 30 days.

Liquidity is distributed on 174 pools split across the following DEXes:

- Balancer V2: $18.75M

- Curve: $15M

- Camelot: $8.95M

- Uniswap V3: $260k

As a conservative measure, we can simulate the expected slippage conditional on a decrease of 30% of wstETH’s on-chain liquidity over the next 30 days:

| Trade size | Actual Slippage (%) | Adjusted Slippage (%)* |

| $100K wstETH | -0.1% | -0.14% |

| $500K wstETH | -0.15% | -0.21% |

| $1M wstETH | -0.21% | -0.3% |

| $2M wstETH | -0.37% | -0.52% |

| $5M wstETH | -0.84% | -1.2% |

* Conditional on 30% decrease in liquidity and assuming the same liquidity distribution profile

It is worth noting that wstETH on Arbitrum can’t be claimed for stETH, contrary to its counterpart on Ethereum. Thus, wstETH liquidity is strictly limited to liquidity of the token itself. Although a mitigating factor is Arbitrum’s wstETH price is usually kept in line with mainnet by market markets.

Centralization

wstETH total supply on Arbitrum as of April 6, 2023 is standing at 32k wstETH ($66.7M).

The holder base is well diversified and centralization risk is relatively low given how distributed wstETH is on mainnet and on Arbitrum.

Proposed Parameters

Over the following section, we’ll review the parameters as proposed by @plpmtech

- Minimum collateral ratio: 150%

- VST Mint cap: 600K VST

- Liquidation bonus: 15%

- Vesta reference rate: 3.0%

Mint cap

It is our assessment that setting the Mint cap at 600K VST is appropriate given the current wstETH on chain liquidity and would allow stability pool depositors to swap wstETH for stables without incurring too much slippage.

Let’s suppose a worst case scenario where one user would mint the whole 600K VST against wstETH and be liquidated. Under that scenario, the stability pool depositors would receive wstETH in exchange for their VST. Stability pool depositors could then exchange wstETH for USDC at 0.15% slippage given the current on-chain liquidity. Even if wstETH on-chain liquidity decreases by 30% over the coming weeks, slippage to execute a 600K trade would be about 0.21%. Stability pool depositors would then swap USDC to VST in order to profit from the liquidation.

In most cases, only part of the 600K would get liquidated as wstETH depositors will mint VST at different collateralization levels.

600K VST represents about 9% of the current VST supply. If the mint cap is reached due to strong market demand, we could reassess wstETH on-chain liquidity and volatility profile to increase the cap.

Liquidation Penalty

It is our assessment that the proposed Liquidation penalty of 15% is likely to compensate stability pool depositors sufficiently to cover wstETH liquidation costs.

A stability pool depositor will incur the following costs when liquidating wstETH for VST:

- Slippage selling wstETH for USDC and USDC for VST.

- As mentioned previously the slippage cost of selling wstETH for VST is sub 1% for a trade size of $600K which implies the whole mint cap would have to be liquidated at once.

- Gas costs

- We estimate the gas liquidation cost at 0% assuming the gas compensation will cover this cost. The only gas cost the liquidator will have to pay is gas to swap wstETH for VST.

- Oracle price skew

- Based on historical data, the price skew between the Oracle price and the market price can be as large as 1.6%. This means that in a worst case situation a liquidator would have lost 1.6% of the 15% liquidation bonus due to the Oracle price skew.

This means that, based on historical data and looking at comparatives assets, a stability pool depositor should expect to profit for wstETH liquidations assuming the stability pool depositors convert wstETH for VST as soon as an account is liquidated. Based on the historical maximum drawdowns of wstETH and similar assets the liquidator is expected to have a sufficient buffer to profit from liquidations.

If the stability pool is not sufficiently large for wstETH then the VST staking module would execute the liquidation.

We think the proposed liquidation penalty of 15% is adequate for the time being.

Collateral Ratio

The minimum collateral ratio protects the protocol against large decreases in collateral asset prices. We think the proposed parameter of a 150% minimum collateral ratio is appropriate at the current time given wstETH and similar asset historical volatility profiles.

The proposed 150% minimum collateral ratio and the 15% liquidation penalty imply that the protocol has an additional 35% buffer. This buffer would protect the protocol in a situation where the wstETH price would decrease rapidly before liquidations can occur

To avoid the creation of bad debt, the protocol should set its minimum collateral ratio at a point where it covers for the 15% liquidation penalty and also protects the protocol against a large decrease in the collateral asset price.

Given a 150% collateral ratio and 15% liquidation discount, the buffer left for covering the asset price drawdown until a liquidation is executed is:

(1 / (150% - 15%)) - 1 = -26%

The worst maximum 1 hour drawdown of wstETH in the last year was -9.46%. This is well within the -26% price decline the buffer would have protected the protocol against.

It is our assessment that the proposed parameter of 150% minimum collateral ratio for wstETH is likely to protect the protocol against a large decrease in the wstETH collateral price even if no liquidation occurs for at least 1 hour.

We think the minimum collateral ratio for wstETH could be potentially lowered following the Shanghai update as it will make stETH redeemable for ETH on Mainnet. The ability to redeem stETH will make the volatility profile of wstETH even more similar to ETH as it will mitigate wstETH liquidity risk. The additional risks of holding wstETH compared to ETH post Shanghai will be mainly slashing risk and smart contract risk.

Vesta Reference Rate

In order to properly evaluate the suggested Vesta Reference Rate, we can compare wstETH liquidity and volatility profile against other assets that are already onboarded on Vesta.

We think the proposed Vesta reference rate of 3.0% is very conservative as an initial parameter and could be lowered in the future especially post Shanghai update.

Conclusions & Next Steps

Our analysis demonstrates that current parameters are conservative enough to safely list wstETH as a collateral asset on Vesta. As per our measurements, the current mint cap, collateral factor and liquidation discount are conservative.

We could reassess parameters in the following months if needed as we gather more information about the actual wstETH utilization on Vesta.

References

-

wstETH Token (Arbitrum) | Warden Finance - https://www.warden.finance/tokens/wsteth?chain=arbitrum

-

wstETH Holders | Arbiscan - https://arbiscan.io/token/0x5979D7b546E38E414F7E9822514be443A4800529#balances