Hey Vesta Community,

This proposal aims to add Lido’s wrapped stETH (wstETH) as a new collateral type on Vesta. wstETH is created by depositing stETH into the stETH wrapper in Lido. Wrapping stETH creates a DeFi-compatible version of the stETH token, allowing for easier integrations with DeFi protocols. This would provide ETH stakers with an opportunity to not only leverage their staked ETH position but also earn original daily rewards generated by stETH. Furthermore, Vesta would benefit from the increased diversity of supported assets and attracting wstETH holders for TVL growth.

Motivation

- Deep liquidity: The current total supply and market cap of wstETH on Arbitrum is nearly 30K and $60M. Also, there are more than 24K wstETH holders on Arbitrum.

- Diversification: Adding wstETH as collateral will enhance the diversity of assets supported by Vesta, and increase the popularity and volume of VST.

- Easy to operate: wstETH can be easily bridged to Arbitrum via the official Arbitrum bridge.

- Enhanced utility: Currently, wstETH on Arbitrum is mostly used in yield farming pools on Curve and Balancer. Lending as collateral to mint VST would be a new and attractive usage. Therefore, it will not be hard to gather TVL at the early stage.

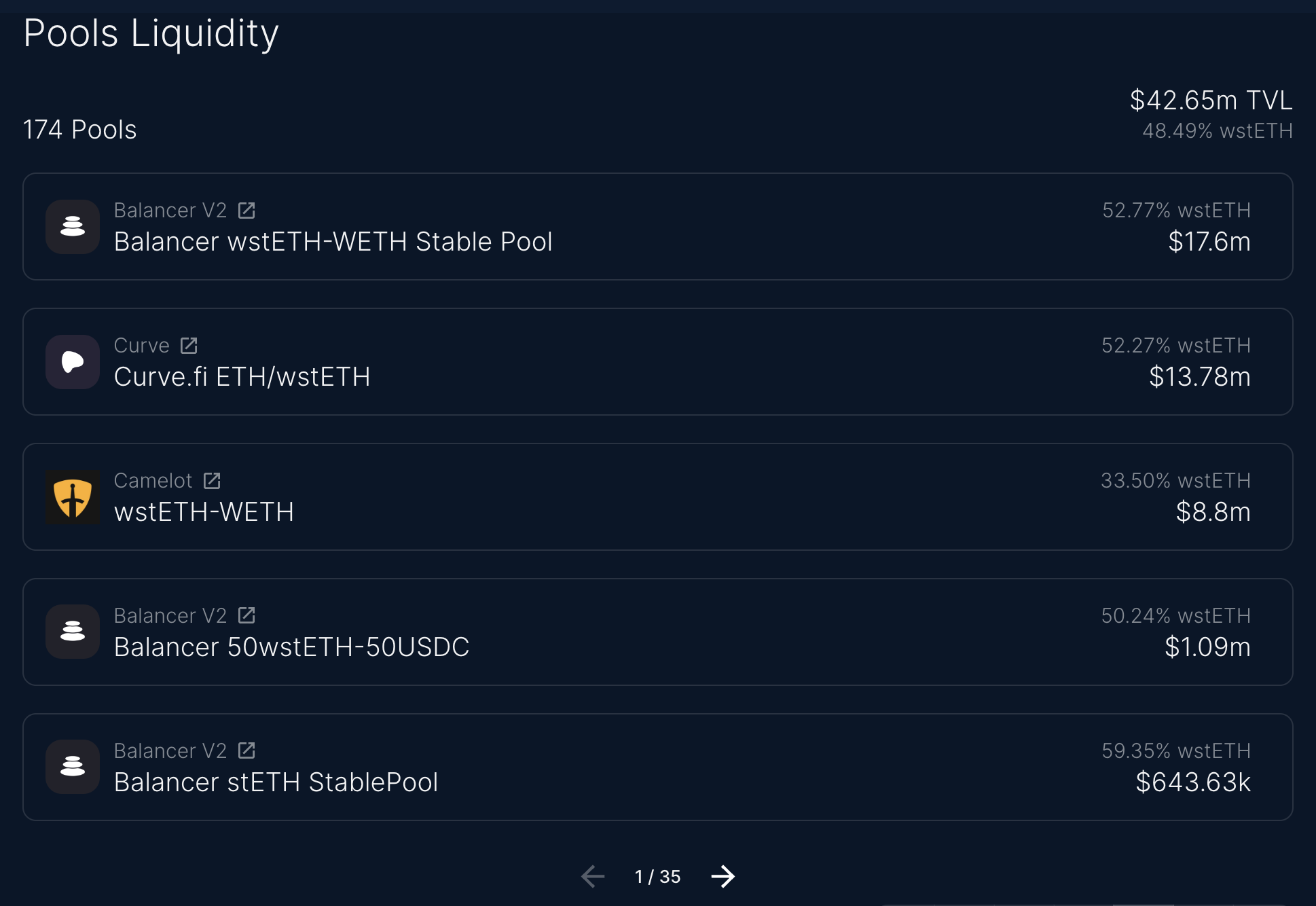

Lido’s wrapped stETH

The link to the main project Github repo for Lido Finance:

The verified wstETH contract:

0x5979d7b546e38e414f7e9822514be443a4800529

The age of the token on Arbitrum:

- 5 months (October 2022)

The number of transactions in token contracts to date: 935,986

Token supply: 29,827.05

Market cap: $59,840,525.06

The chart below shows the total wstETH bridged to Arbitrum since its launch on Arbitrum.

Proposed Parameters

- Collateral Type: wstETH

- Minimum Collateral Ratio: 150%

- Debt Ceiling:

- Initial: we may start the pool with 600K of the mint cap (roughly 1% of the current market cap)

- Scaling: we aim to scale the mint cap with the growth of the wstETH market cap on Arbitrum

- Liquidation Penalty: 15%

- Vesta Reference Rate: using βcollateral = 0.75%

- Oracle: Chainlink or similar decentralized oracle network. There’re live Chainlink wstETH/stETH rate feeds for Arbitrum.

Risk Assessment

Smart contract risk

Lido has been audited multiple times with no critical issues found. There is also an independent audit by MixBytes for wstETH token with only 5 warnings and all have been fixed or acknowledged by Lido’s team.

Counterparty risk

Holders of the token on Arbitrum: 24,553

The decentralization level of the governance of the protocol that issues this token:

Lido is managed by the Lido DAO, which governs all Lido governance and network decisions. For example, the decision of bridging wstETH to Arbitrum is made by LDO holders by voting on Snapshot. For security, Emergency Brakes multi-sigs have been set up on Arbitrum. Also, a portion of the ETH staked via the Lido DAO is held across multiple accounts backed by a multi-signature threshold scheme to minimize custody risk.

Upgrade of token contract:

Lido is going to present V2 upgrade as Shanghai edges closer, but there is no proof that the token contract will be upgraded.

Market risk

wstETH is subject to price volatility, but its high relationship with ETH and our 150% of liquidation ratio and 600K of starting mint cap should provide adequate protection against market fluctuations.

The depth of liquidity on this token: wstETH is mainly based on the ETH staked ($10.5B) and stETH wrapped ($2.7B) on Lido.

Oracle: we’ll make use of a reliable and decentralized oracle network like Chainlink to ensure accurate and tamper-proof price feeds for wstETH.

Token Volatility: Volatility is obviously close to ETH as the two are highly linked, the 30D Volatility is 0.62 for wstETH and 0.58 for ETH according to Messari.

Future emission schedule: wstETH can be minted infinitely as long as stETH is wrapped in Lido, but limited by the staked ETH amount.

Timeline

This poll/discussion period will be live for seven days and if passed, the official voting will commence immediately and will take place over three days.

It is a sensible and strategic move to add wstETH as collateral on Vesta. Our protocol would benefit from the diversity and increased usage in the Arbitrum ecosystem. Furthermore, the new collateral to mint VST would draw more wstETH to be bridged to Arbitrum. We welcome feedback and discussion from the Vesta community before moving forward with the implementation of wstETH as collateral.